Last Updated on December 30, 2025 by Ewen Finser

As a CPA, I’ve watched countless entrepreneurs hit a six-month wall — not because of their product, but because of a back office built on a Frankenstein stack of disconnected software.

They rely on separate gateways, fraud tools, and accounting systems that simply don’t talk to one another, creating a data silo that bleeds cash through unrecovered chargebacks and wastes endless hours on manual reconciliation. When your financial infrastructure is fragmented like this, you aren’t analyzing a business… you’re just playing detective with incompatible CSV files.

One increasingly popular solution is a shift toward smart processors that act as financial ERPs rather than just pipes moving money. These platforms consolidate the transaction, risk management, and operational reporting into a single, unified environment, effectively closing the gap between the sale and the ledger.

And after spending the last quarter looking over APIs, fee structures, and dashboards of the current landscape, I’ve identified the top five Payment Processors with ERPs Built In that go beyond basic payments to actually help you run your business.

TL;DR: While Stripe remains the standard for developers and Square dominates physical retail, I find that Luqra currently offers the best balance of enterprise-grade data visibility and cost transparency for high-growth e-commerce brands, as it delivers the robust control of an ERP without the complexity or bloat.

What I Look For in Payments + ERP

Traditionally, an ERP like SAP or Oracle was a massive, expensive software suite that managed your inventory, HR, accounting, supply chain, reporting, etc. Payments were just a tiny plug-in on the side.

In my opinion, that model has flipped. For digital merchants, cash flow is the supply chain. The movement of money is the operation. Therefore, modern processors have had to evolve, absorbing the functions of an ERP directly into the payment flow.

So when I evaluate payments + ERP, I look for four pillars:

- Unified Data: Does the gateway talk to the risk engine? Does the risk engine talk to the reporting suite?

- Reconciliation Intelligence: Can the system automatically match a batch deposit to the individual transactions that comprise it, including refunds and chargebacks?

- Operational Logic: Can I manage inventory, customer disputes, and recurring billing logic inside the platform?

- Financial Transparency: Can I see my true effective rate and COGS in real-time?

With that criteria set, let’s look at the contenders.

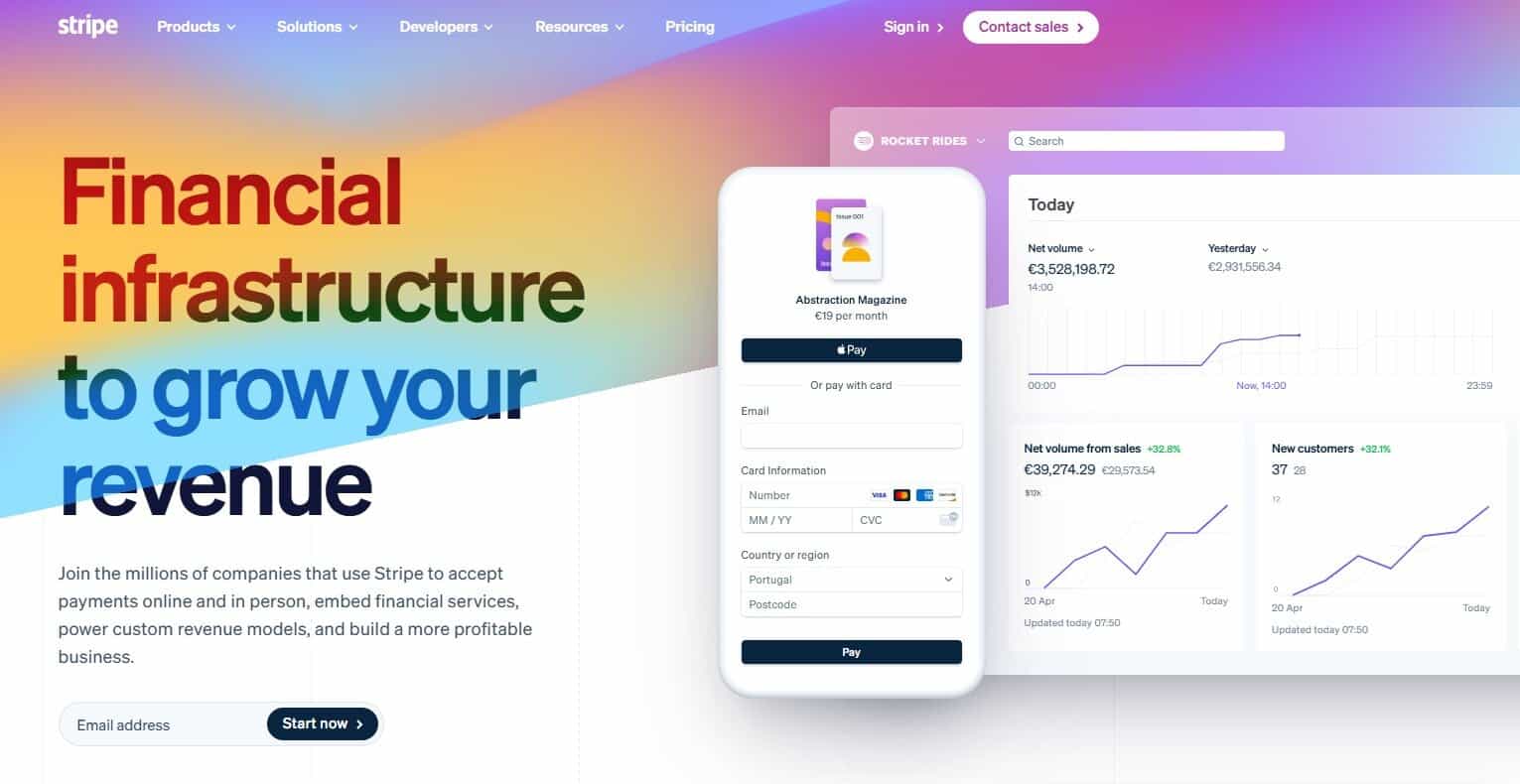

1. Stripe: The Developer’s Dream, the Accountant’s “It’s Complicated”

You can’t write a list about payment processing without mentioning Stripe. They effectively invented the modern API-first economy. And over the last few years, they’ve expanded into a modular financial ecosystem that rivals many mid-market ERPs.

Stripe’s “ERP,” however, isn’t a single dashboard; it’s a collection of modular products that you stack together like Lego bricks. But like Lego bricks, it’s surprisingly strong.

- Stripe Sigma: This is their standout feature for data nerds. It allows you to write SQL queries directly against your transaction data. Instead of downloading a spreadsheet, you can programmatically ask, “Show me all transactions from California over $50 that were refunded in Q3.”

- Stripe Tax & Revenue: These modules handle the incredibly complex logic of global sales tax collection (VAT/GST) and revenue recognition (ASC 606). For SaaS companies, this is a lifesaver.

- Stripe Atlas: While not strictly processing, Atlas handles business incorporation, effectively working as an ERP for startups.

Stripe is magnificent if you have a developer team. The data is clean, the API is flawless, and the integrations are endless. However, from a cost accounting perspective, Stripe can be dangerous. Their base pricing is a flat rate (which is often higher than interchange-plus for high-volume merchants), and every single ERP-like module you add costs extra.

Want advanced fraud protection (Radar)? That’s a fee. Want tax automation? That’s a fee. Want Sigma reporting? That’s a monthly infrastructure fee plus a per-query cost.

I’ve worked with clients who started with Stripe because it was easy, only to realize three years later that their effective processing rate had ballooned to 4% just because of all the add-ons.

- Strengths: Infinite customization, global compliance tools, unparalleled documentation

- Weaknesses: Modular pricing leads to fee creep, support is largely automated/email-based, flat-rate pricing is inefficient for high average order values

Best For: SaaS companies, startups, and businesses with dedicated engineering teams.

2. Square: The “Business in a Box” for Retail

If Stripe is for the code-savvy, Square is for the design-conscious. Square revolutionized POS for coffee shops, but they have built one of the most cohesive operational ERPs for retail and inventory-heavy businesses.

The genius here is that they don’t make you integrate an ERP; they just give you one.

- Inventory & COGS: Square for Retail tracks your stock levels in real-time. If you sell a shirt in-store, it is deducted from your online inventory instantly. It even tracks Cost of Goods Sold, allowing you to see profit margins per item, not just revenue.

- Team Management: This includes timecards, permissions, and even payroll (for an extra fee, of course).

- Customer Directory: Square builds a CRM profile for every card swipe, tracking customer loyalty and purchase history automatically.

It’s the most user-friendly platform on this list. The interface is beautiful, and the reporting is intuitive. You don’t need a degree in finance to understand a sales summary report.

The downside? It’s a walled garden. Square does not play well with others, so if you want to use a different accounting tool or a specialized loyalty program, you might struggle to get data out of Square. Furthermore, their processing fees are generally high and non-negotiable; you’re paying a premium for the convenience of having the hardware and software combined.

For a $5M/year e-commerce merchant, Square is likely too expensive and too restrictive. But for a Main Street boutique with an online store, it’s a lifesaver.

- Strengths: Seamless hardware/software integration, excellent inventory management, zero setup time

- Weaknesses: High transaction fees, difficult to migrate away from, lack of advanced B2B features

Best For: Brick-and-mortar retail, restaurants, and omnichannel boutiques.

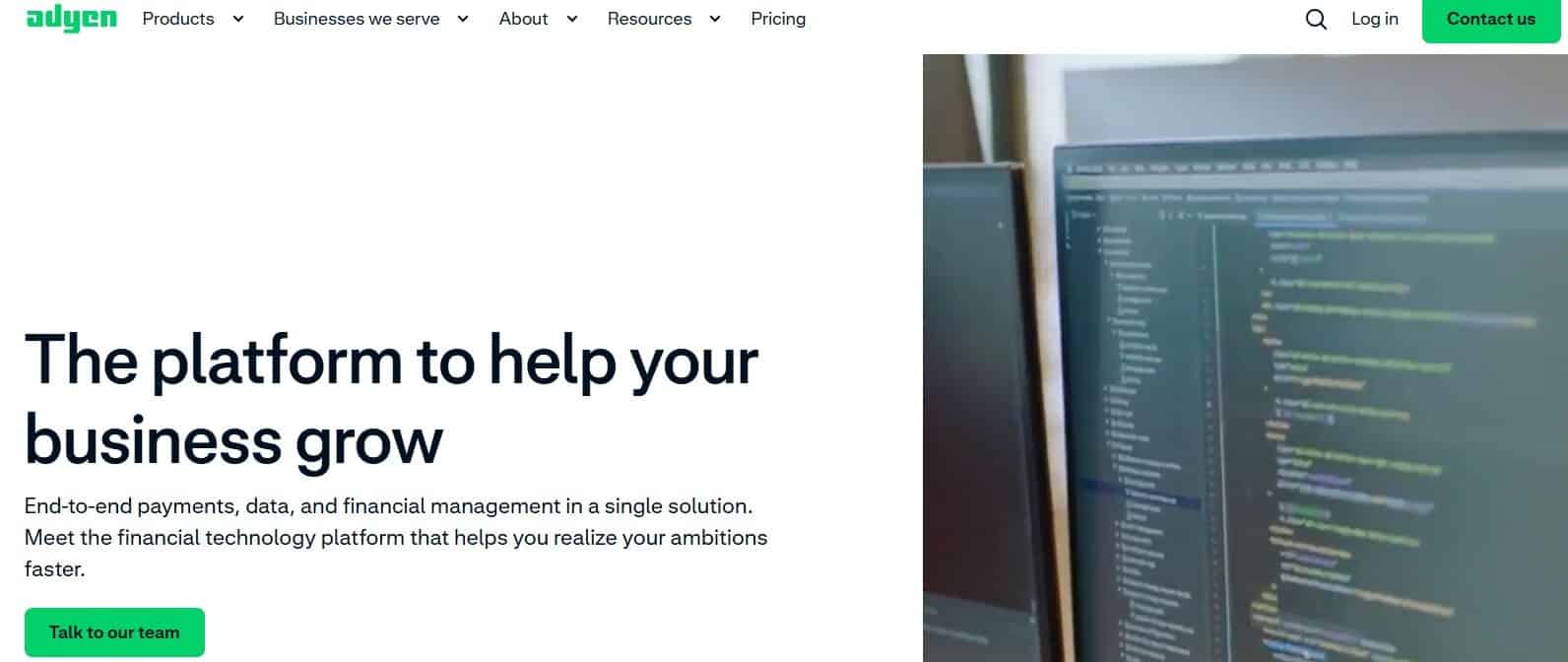

3. Adyen: The Enterprise Heavyweight

If you’re processing $500 million a year, you don’t use Square, and you probably don’t use Stripe. Chances are, you use Adyen, the platform behind Uber, Spotify, and eBay.

It’s less of a tool and more of a financial infrastructure that aims to create a unified commerce environment:

- Global Acquiring: Adyen replaces the entire stack (the gateway, processor, and acquiring bank). This gives them visibility into data that other processors simply don’t have.

- Revenue Protect: Their risk engine is built on global data across industries, allowing for highly sophisticated fraud rules that adapt in real-time.

- ShopperDNA: This is their version of a CRM, linking payment methods to user identities across channels (web, mobile, in-store) to create a single view of the customer.

Adyen is an incredible piece of engineering, but it’s also complex. The dashboard is dense and filled with banking terminology that will confuse the average merchant. It’s also not plug-and-play, and integrating it requires a serious project management timeline and a dedicated finance team to manage the reporting.

It’s built for CFOs with deep pockets, not business owners. However, their Interchange Plus pricing model is transparent and optimized for massive volume. They pass through the raw costs and charge a tiny markup.

- Strengths: Lowest fees at scale, single platform for global payments, deep banking data

- Weaknesses: Extremely high barrier to entry, complex integration, overkill for SMBs or mid-market

Best For: Enterprise-level merchants, multi-national corporations, and marketplaces.

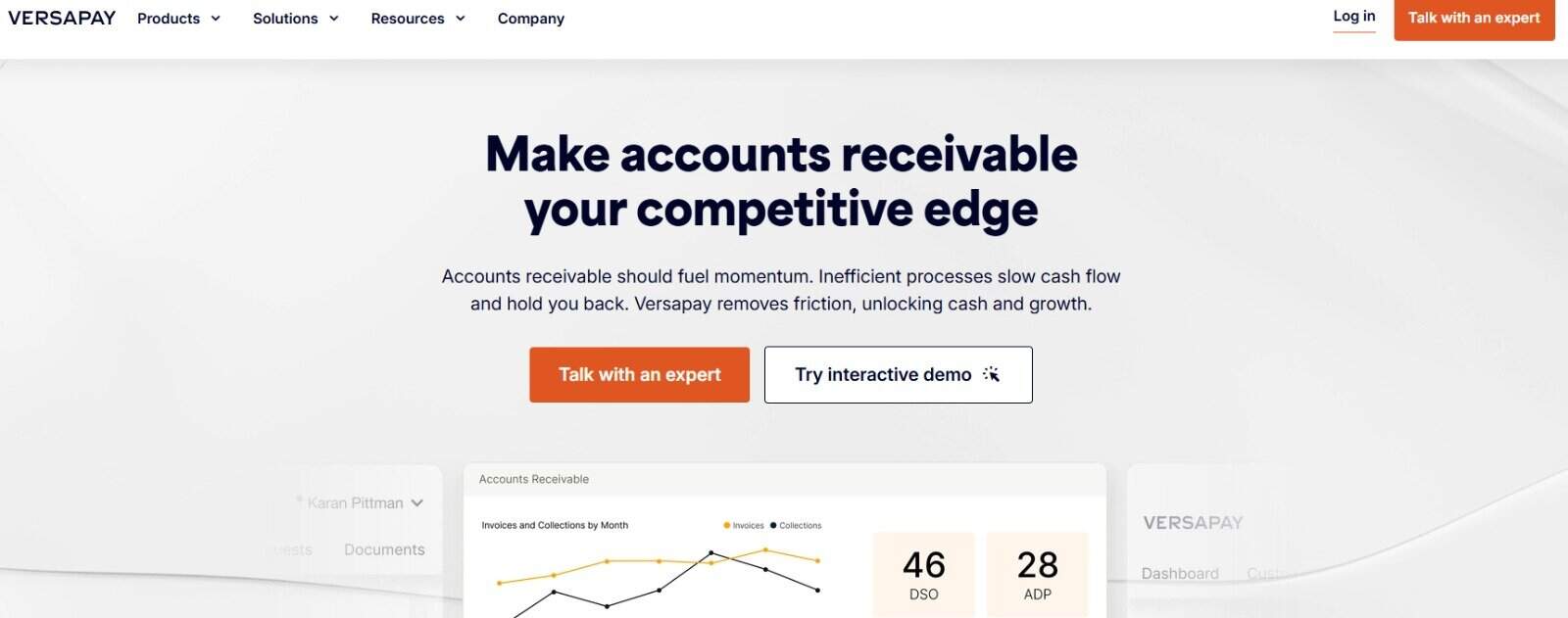

4. Versapay: The B2B Accounts Receivable Specialist

Most payment processors focus on B2C transactions, but what about B2B? What about manufacturers, wholesalers, and professional service firms that send invoices on Net-30 terms? This is where Versapay shines. It’s an ERP-first payment platform designed to automate AR.

Versapay doesn’t just process the credit card; it manages the conversation around the payment.

- Collaborative AR Portal: Versapay provides a portal where your clients can log in to view their invoices. Your customer can also comment on line items (“I didn’t receive this unit,” etc.), resolving disputes before the payment is even made.

- Cash Application: This is the killer feature for accountants. When a payment comes in, Versapay automatically matches it to the correct invoice in Sage, NetSuite, Microsoft Dynamics, etc.

- Collection Automation: Versapay sends reminders and dunning emails automatically based on the invoice due date.

If you run a business that lives and dies by days sales outstanding, Versapay is a game-changer. It reduces the administrative burden of chasing checks and manually posting payments.

However, it’s a specialist tool, and it’s not designed for a high-speed e-commerce checkout flow. So you wouldn’t use Versapay to sell t-shirts on Instagram; you’d use it to collect $50,000 invoices from distributors.

- Strengths: Solves the AR reconciliation nightmare, integrates deeply with major ERPs, improves cash flow velocity

- Weaknesses: Higher setup complexity and not suitable for standard B2C e-commerce

Best For: B2B wholesalers, manufacturers, commercial services.

5. Luqra: The Operational Powerhouse for Growth Merchants

When a new client first told me about Luqra, I was given the chance to dive into its backend and found a suite of offerings that surprised me.

Luqra’s USP is a merchant-first ERP that sits right in the Goldilocks zone: more powerful and transparent than Stripe/Square, but more accessible and agile than Adyen. They’ve taken the approach that the payment processor should be the single source of truth for the business.

- Unified Data Architecture: Unlike legacy systems that patch together a gateway and a processor, Luqra owns the stack. This means when you look at a transaction, you see the gateway data (IP address, device ID) and the banking data (interchange qualification, settlement time) in one view.

- Integrated Analytics & Forecasting: Luqra’s comprehensive analytics and reporting suite helps merchants understand LTV and churn without needing to export data to Excel.

- Risk as Operations: Luqra’s fraud management tools aren’t a black box. They allow merchants to set granular rules and provide detailed evidence for dispute management, which significantly increases win rates on chargebacks.

Luqra distinguishes itself with accountant-ready reconciliation reports that match bank deposits to the penny, saving significant manual labor during the month-end close. Their transparent interchange-plus pricing and unique meat-or-beat rate guarantee provide crucial financial predictability, while their dedicated human support offers a refreshing alternative to the automated bots of competitors.

For merchants in the $1M to $100M range, Luqra delivers the data visibility of an enterprise solution without the complexity, effectively balancing operational control with cost efficiency.

- Strengths: Best-in-class data reconciliation, transparent cost-plus pricing structure, unified risk/analytics dashboard, high approval rates

- Weaknesses: Smaller ecosystem of third-party plugins compared to Stripe

Best For: High-volume e-commerce, subscription models, and digital merchants scaling from 7 to 8 figures.

Final Recommendation: Which Platform Fits Your Business Model?

As a CPA, I don’t believe in one-size-fits-all solutions. Instead, your choice should be dictated by your business model and your transaction volume:

- The Brick & Mortar Hero: If you have a physical store, a few employees, and sell a bit online, Square is unbeatable. The operational friction is near zero.

- The Code Wizard: If you’re building a custom SaaS product with complex, programmatic billing logic, Stripe is the standard. Just keep a close eye on your margins.

- The B2B Powerhouse: If you send invoices and chase checks, Versapay will pay for itself in labor savings alone.

- The Global Giant: If you are the next Uber, go through the pain of setting up Adyen.

However, for pure-play digital merchants tired of flying blind, Luqra stands out as the payments + ERP solution to beat in 2025, prioritizing profit and offering the data transparency and pricing structure needed to protect your margins.

Related read:

The Best Payment Processors for QuickBooks