Last Updated on February 24, 2026 by Ewen Finser

As many business owners have learned, selecting a payment processor for your Shopify store isn’t just a “check the box” technical requirement. As a CPA, I view it as a fundamental strategic decision that dictates the health of your cash flow, the accuracy of your ledger, and the long-term scalability of your margins (I also probably take it a bit more seriously than most business owners). In this day and age, we aren’t just looking at who can “swipe a card” online anymore – that pretty much comes standard out of the box now. We are looking at entire data ecosystems and how the platforms we use can take advantage of the information

If you’re running a Shopify store, you’ve likely been nudged toward their native solutions. But for a growing business, the “easy” path is often the most expensive one once you start to look at the hidden leakages. When the folks I work with ask me for the “best” processor, they usually want the cheapest. Those two things often don’t correlate. My job is to remind them that a 2.9% rate is meaningless if your funds are frozen for weeks by an algorithm that doesn’t understand your business model, or the 2.7% rate vendor holds your funds for three business days.

In this deep dive, we’re going to look at five major players: Shopify Payments, Stripe, Authorize.net, PayPal, and Luqra. We’ll break down the rates, the support (or lack thereof), and the operational reality of living with these systems.

1. Shopify Payments: Well…Duh.

Shopify Payments is the default choice for a reason: it’s built directly into the admin. It’s a no-brainer that it made the list. From an accounting perspective, the integration is undeniably clean. Your payouts, refunds, and chargebacks all live in the same dashboard as your orders. There’s no “middleman” software to sync, which reduces the margin for error in your reconciliation process.

The Financials

Shopify’s pricing is tiered based on your subscription plan. As of 2026, the rates generally look like this:

- Basic Plan: 2.9% + $0.30

- Shopify (Grow) Plan: 2.7% + $0.30

- Advanced Plan: 2.5% + $0.30

The hidden cost here is the Third-Party Transaction Fee. If you choose not to use Shopify Payments, Shopify charges you an extra 0.5% to 2.0% per transaction just for the privilege of using a different gateway. This is a classic walled garden tactic that makes other processors look more expensive than they actually are.

What They Excel At

- Speed of Implementation: You can be up and running in an afternoon.

- Shop Pay: Their proprietary accelerated checkout has some of the highest conversion rates in the industry.

- Unified Reporting: For a solo founder, having one 1099-K and one dashboard is a massive time-saver at tax time.

The Downsides

Shopify Payments is essentially a white-labeled version of Stripe. They are a Payment Facilitator. This means they aggregate thousands of merchants under one master account. Because they take on the risk of all those merchants, they are notoriously “trigger-happy” with account freezes, in my opinion.

I’ve had business owners get frozen funds notifications because of a sudden spike in sales, which should be a good thing! But to an automated risk algorithm, a sales spike looks like fraud. Resolving these issues often involves a lot of automated support tickets, which is not super transparent and somewhat frustrating.

2. Luqra: The Hybrid Strategist

Next, we have Luqra. I think growing merchants may want to consider Luqra when they outgrow the “simplicity” of Shopify Payments but don’t want the coldness of the larger Silicon Valley giants. Luqra positions itself as a full-stack processor that adds a layer of lite ERP functionality.

The Financials

Luqra operates on a “Meet or Beat” model. While Shopify and Stripe have “take it or leave it” pricing, Luqra’s team actually looks at your processing history.

- Standard Rates: Often start around 2.0% to 2.3% + $0.10, depending on volume. These types of rate would materialize if you were previously using an interchange plus model with a modest amount of volume.

- Transparency: They are vocal about “zero hidden fees” and no surprise rate increases, which is a breath of fresh air for anyone who has ever tried to decipher a monthly merchant statement.

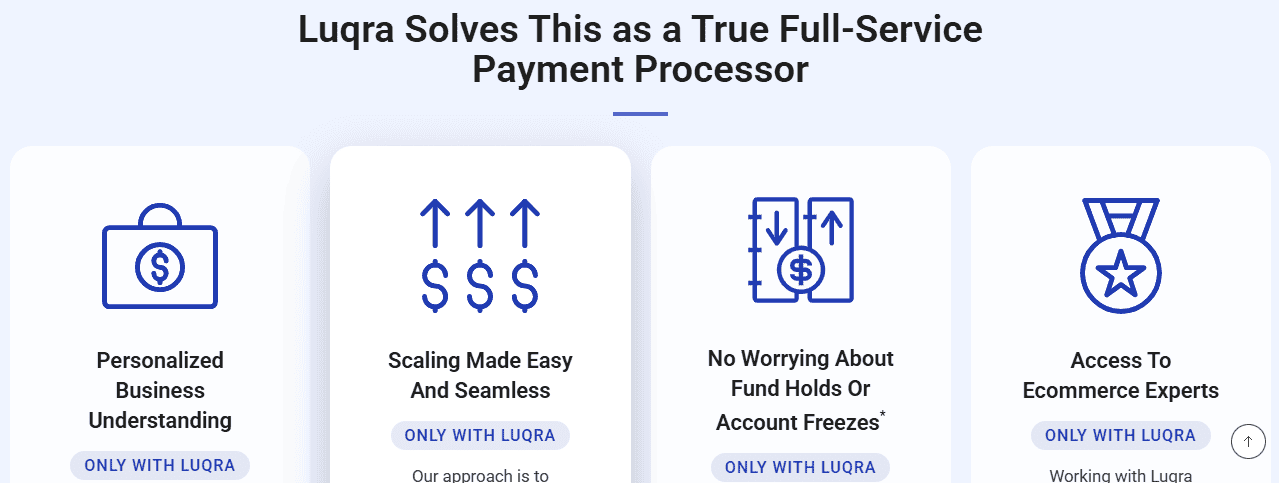

What They Excel At (The “ERP” Advantage)

What makes Luqra interesting to me as an accountant isn’t just the rate. They offer an ERP system that goes beyond just processing, so you can keep a ton of different reports and data under one umbrella. Some other features are:

- Human-Led Underwriting: Unlike the bots at Shopify or Stripe, Luqra uses actual humans to underwrite your account. This means they understand your business before you start selling. The result? Zero account freezes for legitimate merchants. They don’t panic when you have a big Black Friday sale and exceed expectations.

- Integrated Chargeback Management: Instead of you manually fighting every dispute in the Shopify admin, Luqra has built-in tools that proactively manage and mitigate fraud before the chargeback even happens.

- Financial Hub: Their ERP back-end bridges the gap between your sales data and your operational data. It provides a “single pane of glass” for managing inventory, fraud, and payments. For a business that is scaling, this is the difference between “running a store” and “managing a company.”

What They’re Not As Good At

- Brand Awareness: They aren’t as famous as PayPal. You won’t find a “Pay with Luqra” button on the front end. They work behind the scenes to power your existing Shopify checkout, which is where they belong.

- Setup Time: Because they do real underwriting to protect you from future freezes, the onboarding takes a bit longer than the “30-second” signup at Shopify. But in my experience, the extra setup is worth avoiding a month of frozen cash.

3. Stripe: The Developer’s Darling

Stripe is the engine under the hood of much of the internet. If you have a custom-built headless Shopify store or a complex subscription model, Stripe is usually the first name on the list.

The Financials

Stripe’s standard “Pay-as-you-go” pricing is 2.9% + $0.30. However, they are famous for fee creep. You’ll pay extra for:

- International Cards: +1.5%

- Currency Conversion: +1%

- Stripe Radar (Fraud Tools): $0.05 per transaction

- Chargeback Protection: Often 0.4% per transaction

What They Excel At

- Customization: Their API is the gold standard. If you want a checkout experience that is pixel-perfect and unique, Stripe is the way to do it. You better have some good developers on hand, though, because otherwise you won’t be able to take full advantage of the platform.

- Analytics: “Stripe Sigma” allows you to run SQL queries on your payment data. For a data-driven CFO, this is pure gold.

- Global Reach: They support almost every currency and local payment method.

What They’re Not As Good At

- Customer Support: Much like Shopify, Stripe relies heavily on automated systems. If your account gets flagged, you aren’t calling a “Stripe representative” on their cell phone. You are waiting for an email or talking to someone who has to read from a script.

- Complex Reconciliation: Because Stripe has so many “add-on” fees, reconciling your bank statement to your Shopify orders can become a nightmare without sophisticated accounting software or someone to spend a ton of time looking everything over.

4. Authorize.net: The Old Guard

Owned by Visa, Authorize.net is one of the oldest players in the game. Unlike the PayFacs mentioned above, Authorize.net is a gateway that connects you to a dedicated merchant account.

The Financials

This is where it gets “old school.”

- Monthly Gateway Fee: $25

- Per Transaction Fee: 2.9% + $0.30 (if using their merchant account)

- Batch Fee: $0.10 per day

What They Excel At

- Stability: Because you often have your own dedicated merchant account, you go through a more rigorous “underwriting” process at the start. It’s harder to get approved, but once you are, your account is much less likely to be frozen than with a typical payment facilitator.

- Custom Fraud Filters: They offer highly granular control over which transactions you accept or decline.

What They’re Not As Good At

- User Interface: The dashboard looks like it hasn’t been updated since 2012. And ya know what, that’s okay because the platform is a reliable workhorse that gets things done.

- Integration Friction: While it integrates with Shopify, it’s not as “plug and play” as the others. You’ll be managing two separate logins and two separate support teams.

5. PayPal: The Trust Factor

You cannot ignore PayPal. Even if you hate their fees, your customers love the “PayPal” button. For many international shoppers, it’s the only way they feel safe buying from a US-based store.

The Financials

PayPal is consistently the most expensive option.

- Standard Online Rate: 3.49% + $0.49

- International: They take a massive bite out of currency conversion (usually around 3-4% above the mid-market rate).

What They Excel At

- Conversion: Including PayPal as an option can increase checkout conversion by up to 30% in certain niches. It’s also super convenient, and even I love PayPal because I can just click a button and send the money out of my account.

- Buyer Protection: This is why customers love it. They know they can get their money back if you don’t ship the product.

What They’re Not As Good At

- Seller Protection: PayPal is notoriously biased toward the buyer. In a dispute, the merchant often loses by default unless their documentation is flawless.

- Fund Holds: PayPal is famous for “21-day holds” on new accounts or high-volume stores. As a CPA, I find PayPal the most difficult to manage for cash-flow forecasting because of these unpredictable reserves.

So, Who Are We Choosing?

If you are doing under $10,000 a month in sales, stay with Shopify Payments. The convenience is worth the extra 0.5% in fees, and the risk of a major fund freeze is relatively low at that volume.

If you are a developer or a tech-heavy startup, go with Stripe. The API flexibility is unmatched, provided you have the technical staff to manage the complexity and the margins to absorb the fee creep. Just be prepared to get to work to take advantage of the platform in full.

However, if you are a scaling merchant (doing $50k+ per month) and you are tired of being treated like a number by automated bots, Luqra is the move. From my perspective, the “Meet or Beat” pricing combined with the ERP back-end provides the best balance of margin protection and operational sanity. Their focus on transparent pricing and real-time approvals means you spend less time fighting with your processor and more time looking at your P&L.

In the end, payment processing shouldn’t just be a cost center. It should be a data source that helps you run a better business. Choose the partner that treats your cash flow with the same respect you do.