- The Bottom Line Up Front:

- My Top Eight Picks and Why:

- 1. Melio

- 2. Stripe

- 3. PayPal

- 4. Square

- 5. Authorize.net

- 6. Braintree

- 7. Adyen

- 8. Amazon Pay

- Choosing the Right Payment Gateway: My Thoughts

- Where Each Gateway Excels

- Hidden Costs and Common Payment Pitfalls

- Bringing It All Together

- Final Thoughts

Last Updated on March 2, 2026 by Ewen Finser

As many small business owners know, money movement (and management) is one of the most important, and most stressful, parts of day-to-day operation. In my work as a CPA, I’ve worked with countless clients across many industries: retail shops, restaurants, online merchants, contractors, and service providers. If there’s one thing I’ve learned, it’s that choosing the right payment gateway can majorly improve efficiency!

However, the challenge is choosing a provider that balances cost, reliability, customer experience, and accounting workflow. Some gateways shine with e-commerce, others with brick-and-mortar. Others offer rock-solid integration into accounting systems, which is something I pay special attention to in my line of work.

The Bottom Line Up Front:

Truth be told, the best payment gateway for a small business depends on how you operate. There is no one-size-fits-all solution. If you run a retail shop or restaurant, Square is hard to beat. If you’re building an online store or subscription service, Stripe leads the pack. PayPal and Amazon Pay boost checkout conversions by adding familiar options for customers.

For service-based businesses, contractors, and B2B operations, Melio edges out the competition by combining free ACH transfers, flexible credit card payments, and smooth accounting integration. From my perspective, it’s the platform that most consistently simplifies cash flow and bookkeeping, which I feel are two areas small business owners can’t afford to get wrong.

My Top Eight Picks and Why:

With that quick overview out of the way, let’s get into the tools themselves. Below are my top eight payment gateway picks for small businesses, along with what each one does best and who it’s a good fit for.

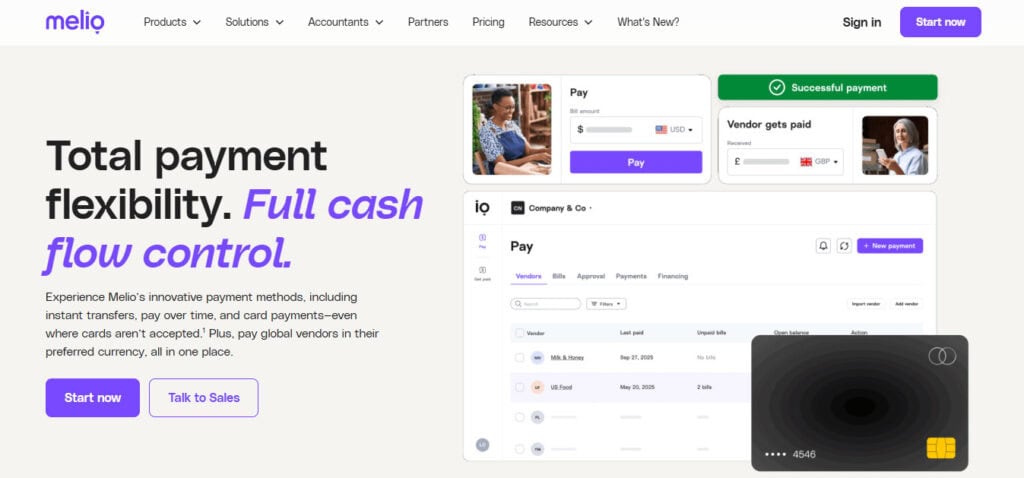

1. Melio

I’ll start with the one I recommend most often: Melio.

Melio stands out because it was built with small business owners in mind. Unlike some platforms that started enterprise-first and later scaled down, Melio, to me, has always catered to the smaller operator who needs flexibility without high fees.

Key Strengths:

- Free ACH payments (the number depends on your tiered plan)

- Ability to pay vendors with a credit card, even if they don’t accept cards. This is SUCH a game changer if you’re tightly managing cash flow.

- Clean, intuitive dashboard that doesn’t feel like enterprise software.

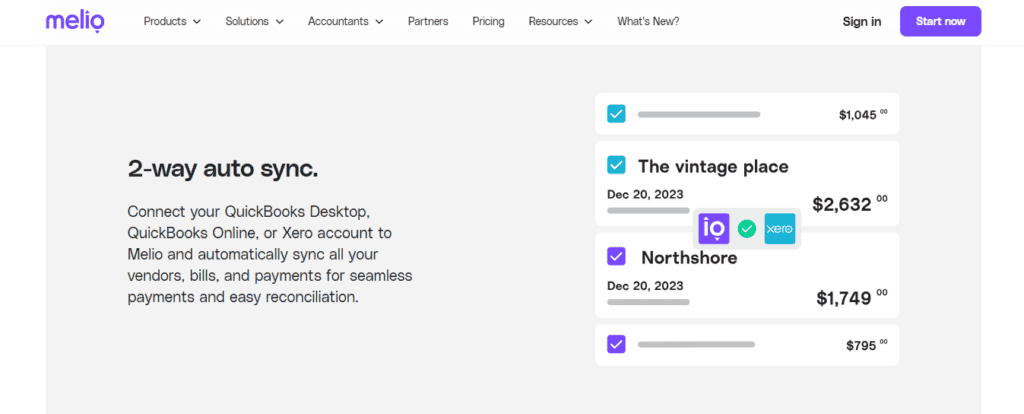

- The ability to sync to Intuit’s QuickBooks Online

- AI-driven bill capture and smart suggestions for coding and categorizing expenses, helping you minimize repetitive tasks and improve accuracy in your accounts.

As a CPA, one of my biggest headaches is when clients use tools that don’t sync properly with their accounting software. Melio solves this issue by automating much of the bookkeeping process. Bills, receipts, and vendor payments flow directly into the ledger, which is game-changing. It should be noted at this time, the Bill Pay Feature powered by Melio within QBO has been discontinued as Intuit wanted to focus on QBO Bill Pay Features. Melio acts as a standalone platform that syncs to QBO now.

In my opinion, the biggest downside is that it isn’t designed for heavy retail or point-of-sale operations. If you run a busy coffee shop with hundreds of card swipes a day, you may want to consider an alternative platform. But for B2B, contractors, professional services, and e-commerce vendors, Melio is hard to beat.

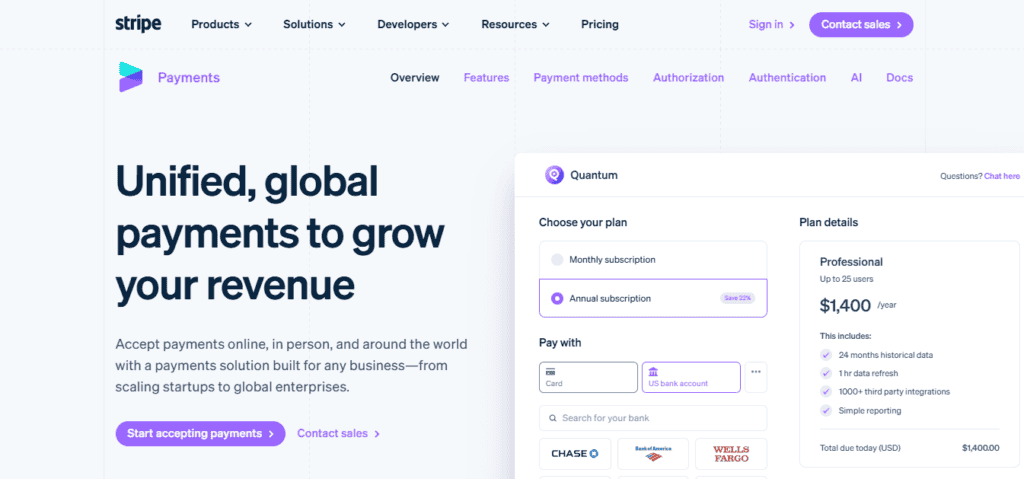

2. Stripe

Stripe has become almost synonymous with online payments. When I work with tech-forward clients, they nearly always bring up Stripe first, and for good reason.

Key Strengths:

- Excellent for e-commerce, SaaS, and online marketplaces.

- Strong developer tools and APIs.

- International payment support in 135+ currencies.

- Broad integrations with e-commerce platforms like Shopify and WooCommerce.

The biggest advantage is flexibility. If your business runs online, Stripe can probably be molded to fit your model. I’ve seen clients build entire subscription platforms, booking systems, and digital marketplaces on top of Stripe.

The drawback is complexity and cost. Unless you have a developer on hand, setup can feel overwhelming. Stripe also charges slightly higher processing fees than some competitors, especially for international transactions. Still, if you’re online-first and want to scale globally, Stripe is one of the strongest options.

3. PayPal

PayPal has been around long enough to be considered the veteran of online payments. While it sometimes gets dismissed as outdated, I still see plenty of clients using it.

Key Strengths:

- Familiarity and trust: customers know and trust PayPal.

- Easy setup for e-commerce and invoicing.

- Strong buyer and seller protections.

- Works well for both small ecommerce stores and freelancers.

Where PayPal shines is consumer confidence. I’ve seen conversion rates jump when businesses add PayPal as a checkout option. Customers trust it, and sometimes that matters more than a small difference in fees.

The downside is that PayPal’s fee structure can be higher than competitors, especially when dealing with international payments. Additionally, its integrations into accounting systems aren’t as smooth as newer entrants like Melio or Stripe.

Still, as a supplement to your main payment processor, PayPal is worth having.

4. Square

Square, like Stripe, is almost always mentioned when onboarding a payment process providers. For brick-and-mortar shops, Square is often the first name that comes up. If you’ve been to a coffee shop or food truck in the last few years, you’ve probably paid through Square.

Key Strengths:

- Hardware and POS system built for in-person payments.

- Flat-rate pricing, easy to understand and relatively affordable.

- No monthly fees for basic plans.

- Add-ons like payroll and scheduling tools are available.

I like Square for its transparency and reporting. Small businesses don’t always have time to parse through fine print with interchange rates. With Square, you pay a flat percentage per swipe, and that’s it.

I’ve had seen clients grow tremendously, from food trucks into multi-location restaurants using Square as their backbone. The ecosystem scales up well, but it does lock you in. Once you’re embedded in Square’s POS and payroll, moving away can be painful.

For service businesses or online-first companies, Square isn’t the best fit. But if you have a storefront and want something reliable, Square is hard to beat.

5. Authorize.net

Authorize.net is one of the oldest gateways still in wide use. I see it most often in traditional retail or among businesses that have been around for a while.

Key Strengths:

- Reliability and security.

- Wide support across ecommerce platforms.

- Flexible recurring billing options.

- Strong fraud detection tools.

The advantage here is stability. Authorize.net has been trusted for decades, and it integrates with just about every e-commerce platform and system.

The downside is that the interface feels dated compared to Stripe or Square. Pricing is also less transparent, with a mix of monthly fees and per-transaction costs.

For businesses that value stability over flash, though, Authorize.net remains a solid contender.

6. Braintree

Owned by PayPal, Braintree is a modern alternative that caters more to tech-savvy merchants.

Key Strengths:

- Strong mobile payment support.

- Easy integration with apps and e-commerce platforms.

- Multi-currency and global support.

- Lower fees for certain transactions compared to PayPal.

Braintree is essentially PayPal’s answer to Stripe. I see it used by businesses that want flexibility but also the backing of a big name. It handles everything from digital wallets like Apple Pay and Google Pay to recurring billing.

For small businesses that are scaling quickly, Braintree offers a good middle ground between developer flexibility and consumer familiarity.

7. Adyen

Adyen isn’t as well-known in the U.S. among small businesses, but it powers payments for major companies like Uber and Spotify.

Key Strengths:

- Global reach, supports almost any payment method.

- Very strong fraud prevention tools.

- Transparent pricing based on interchange-plus.

- Good for businesses with international ambitions.

The drawback is that Adyen is sometimes overkill for very small operators. It’s better suited for businesses that are already selling internationally or plan to.

When I’ve worked with e-commerce companies scaling to Mexico or Canada, Adyen has been a strong option. But for a local retailer or a small contractor, it’s probably more than you need.

8. Amazon Pay

Finally, there’s Amazon Pay. This one has the familiarity of a big name, but if you’re using Amazon Pay, you may as well consider PayPal or another trusted name. The only caveat is if you’re targeting Amazon users to check out with their Amazon account.

Key Strengths:

- Customers can check out with their Amazon account, reducing friction.

- Trusted brand recognition.

- Easy integration with e-commerce stores.

Amazon Pay’s main advantage is consumer trust and convenience. If your customers already have Amazon accounts (and let’s be honest, almost everyone does), checkout is as simple as a click.

The fees are comparable to PayPal and Stripe, and like PayPal, it works best as an additional payment option rather than your sole processor.

Choosing the Right Payment Gateway: My Thoughts

Over the years, I’ve seen clients rush into picking a payment processor without fully considering the long-term impact. Switching later is messy and kind of sucks to do. It can disrupt bookkeeping, confuse vendors, and sometimes cost more in hidden fees.

Here are the key factors I talk through with clients:

- Fee Structure: Flat-rate vs. interchange-plus can change your margins. For very small businesses, simple flat-rate pricing (like Square’s) can reduce stress. As volumes grow, interchange-plus often saves money.

- Accounting Integration: This is where I spend most of my time as a CPA. Some gateways sync with QuickBooks, Xero, or NetSuite seamlessly. Others leave you with a pile of CSV files to reconcile. Melio and Stripe stand out in automation here.

- Flexibility of Payment Methods: Customers expect to pay with cards, ACH, and sometimes wallets like Apple Pay. The more options you provide, the fewer abandoned carts you’ll see.

- Customer Experience: Payments should feel seamless. If your customers get redirected to clunky portals, conversion drops, costing you money.

- Cash Flow Management: Some gateways release funds instantly, others take days. For instance, Melio’s credit card float feature is a subtle but important cash flow lever for service businesses.

Where Each Gateway Excels

Here’s how I’d summarize the sweet spot for each platform:

- Melio: Best for service-based businesses, contractors, and B2B payments.

- Stripe: Best for ecommerce, SaaS, and international businesses.

- PayPal: Best as a supplement to reduce cart abandonment.

- Square: Best for brick-and-mortar retail and restaurants.

- Authorize.net: Best for legacy systems and businesses valuing stability.

- Braintree: Best for mobile-first startups and app developers.

- Adyen: Best for international scaling and enterprise-level ambitions.

- Amazon Pay: Best as an add-on for consumer trust in e-commerce.

Hidden Costs and Common Payment Pitfalls

Something I always caution clients on: fees are never as simple as they look on paper.

For example:

- PayPal often tacks on cross-border fees that add up fast if you’re selling out of the United States.

- Square’s flat-rate pricing is great at low volumes, but can become costly for larger businesses compared to interchange-plus.

- Stripe’s refunds can still incur non-refundable processing fees, which are a painful surprise if you have high return rates.

- Authorize.net has monthly fees that may not make sense for very small operators.

Pay attention to costs. It’s refreshing when a platform like Melio offers things such as free ACH, and card payments carry a clear fee. That’s one reason I find myself recommending it often.

Bringing It All Together

Look, small businesses don’t have the luxury of getting payments wrong. A poor choice can eat into margins, frustrate customers, or tie you up in accounting headaches. Over the years, I’ve seen every possible mistake, from contractors writing physical checks for every vendor bill, to e-commerce shops losing sales because their checkout page felt sketchy.

The good news is that there are great tools out there. Whether you’re selling coffee, building websites, or contracting large projects, there’s a payment gateway that fits.

If I had to rank them for most of my clients, the order would look like this:

- Melio : Practical, flexible, accountant-friendly.

- Stripe: Best for online-first businesses with growth in mind.

- Square : Point-of-sale powerhouse for retail and restaurants.

- PayPal: A trusted name that boosts consumer confidence.

- Braintree: A modern alternative with mobile strengths.

- Adyen: A global tool for ambitious sellers.

- Authorize.net: Reliable, if a bit dated.

- Amazon Pay: A great add-on for e-commerce stores.

Final Thoughts

As a CPA, I tend to look at payment gateways not just as a way to collect money but as a financial infrastructure decision. They touch accounting, cash flow, and customer experience. Choosing the right one is about more than just fees; it’s about picking the tool that aligns with how your business actually runs.

I’ve leaned toward Melio in recent years because it addresses pain points I see most often with small business owners: cash flow, vendor management, and bookkeeping integration. But I’d never say there’s a one-size-fits-all answer. The best payment gateway is the one that saves you time, preserves your margins, and supports your growth.