- Bottom Line Up Front (BLUF):

- 1. Luqra: The Integrated Agility Specialist

- 2. Stripe: The Developer’s Standard

- 3. Adyen: The Global Enterprise Powerhouse

- 4. Helcim: The Transparent Alternative

- 5. Chase Payment Solutions: The Banking Giant

- The Strategic Importance of ERP-Integrated Payments

- Eliminating the "Data Gap"

- API-First Mentality

- Pricing Transparency: Beyond the Effective Rate

- The Complexity of Fees

- The Fraud Frontier: Protecting the Bottom Line

- Surgical Prevention

- Support: The Human Element in a Digital World

- The Boutique Enterprise Model

- Conclusion: Finding Your Growth Partner

Last Updated on February 26, 2026 by Ewen Finser

In the shifting tides of the 2026 digital economy, the merchant account has evolved from a simple bank-side necessity into a complex strategic engine. And in my opinion, for e-commerce brands, the stakes have never been higher. A decade ago, simply being able to accept a credit card was enough. Today, a merchant account must act as a fortress against fraud, a bridge to international markets, and a data-rich portal that informs every inventory and marketing decision a brand makes.

As e-commerce moves toward a more fragmented, omnichannel reality, the “best” merchant account is no longer just the one with the lowest rates. It is the one that offers the highest degree of stability, adaptability, and integration. Merchants are increasingly wary of “enterprise lock-in”, the phenomenon where a business becomes so dependent on a single provider’s proprietary, closed-loop ecosystem that switching becomes a nightmare.

In this comprehensive guide, we will analyze the top merchant account providers for 2026, ranking them based on their e-commerce-specific features, their ability to scale without friction, and their commitment to merchant-centric stability.

Bottom Line Up Front (BLUF):

In 2026, the best e-commerce merchant accounts are defined by their ability to unify payments with operations. While Stripe remains the gold standard for developer customization and Adyen leads for global enterprise scale, Luqra emerges as the top choice for growth-oriented brands seeking a “Financial ERP” that offers enterprise-grade stability without the restrictive lock-ins or technical complexity of legacy systems. By integrating high-level analytics and automated underwriting directly into the gateway, Luqra provides a streamlined, centralized solution that prioritizes cash flow and transparent, meet-or-beat pricing.

1. Luqra: The Integrated Agility Specialist

At the top of our list is a provider that has redefined the mid-market space. Luqra has gained significant traction by positioning itself as the middle ground between the plug-and-play simplicity of entry-level processors and the rigid, bureaucratic complexity of legacy enterprise systems.

The Philosophy of Unified Commerce

Luqra’s primary advantage in the e-commerce sector is its integration of ERP (Enterprise Resource Planning) and analytics directly into the payment gateway. For most brands, these are three separate subscriptions that require complex API handshakes to share data. Luqra treats them as a single system.

For a scaling brand, this means that a sale made on a mobile storefront immediately informs the inventory levels in the ERP and updates the growth forecasting in the analytics suite. In my opinion, this lack of latency offers a competitive advantage in that the speed of information availability is unprecedented.

Stability Without the “Gilded Cage”

What sets Luqra apart from others on this list is its approach to merchant stability. Many processors are known for sudden account freezes or reserve holds during high-growth periods (like a viral marketing campaign). Luqra utilizes a more robust, proactive underwriting model. By performing deeper due diligence during the onboarding phase, they provide a level of account stability usually reserved for enterprises, yet they do so without the multi-year, iron-clad contracts that define the legacy world.

2. Stripe: The Developer’s Standard

It is impossible to discuss e-commerce without Stripe. For years, Stripe has been the gold standard for customization. If you can dream it, you can code it on Stripe (as long as you have the developer skills, which I certainly don’t).

Customization vs. Complexity

Stripe’s “Elements” and robust API library remain the best in the business for brands that want to build a completely bespoke checkout experience. While the tools are powerful, they do require a dedicated engineering team to build and potentially maintain. For a brand that wants to focus on product and marketing rather than managing a complex technical stack, Stripe can feel like too much.

Furthermore, Stripe’s pricing, while transparent, is rarely the most competitive for high-volume merchants. They trade on convenience and developer-friendliness, which often comes at a premium that eats into the margins of a scaling brand.

3. Adyen: The Global Enterprise Powerhouse

If your e-commerce brand is doing $500M+ in annual revenue across forty different countries, Adyen is likely your first call. They are a global powerhouse that excels at navigating the labyrinthine regulations of international cross-border payments.

The Enterprise Weight

Adyen’s strength is also its barrier. Their platform is designed for the Fortune 500. For a mid-market e-commerce brand, one doing between $5M and $50M, Adyen will feel impersonal. The onboarding process is rigorous, and the platform’s interface is built for professional treasury departments rather than entrepreneurial teams. While they offer incredible stability, they represent the “enterprise lock-in” that many modern brands are trying to avoid.

4. Helcim: The Transparent Alternative

Helcim has built a loyal following by being the “honest” processor. In an industry plagued by hidden fees and teaser rates, Helcim’s interchange-plus pricing model is refreshingly clear.

The Mid-Market Fit

Helcim is an excellent choice for businesses that have outgrown the flat-rate pricing of Shopify Payments or Square but aren’t yet ready for a full ERP integration. They offer a great Smarthub that provides decent analytics. However, for brands with a heavy e-commerce focus, Helcim’s gateway can feel basic. It lacks the deep, surgical fraud prevention and the high-velocity funding options that more specialized agile providers offer.

5. Chase Payment Solutions: The Banking Giant

For many, the security of a “Big Four” bank is worth the trade-off in technology. Chase offers the peace of mind that comes with a massive financial institution.

Reliability vs. Innovation

Chase is incredibly stable. Your funds are safe, and the chances of the company disappearing are zero. However, from a technology perspective, they often lag behind. Their e-commerce integrations are frequently built on older architecture, making the user experience feel antiquated compared to modern, API-first platforms. If you value a relationship with a traditional banker over a high-speed analytics dashboard, Chase is a solid, albeit conservative, choice.

The Strategic Importance of ERP-Integrated Payments

As we look closer at why providers like Luqra are ascending in the 2026 rankings, we must look at the convergence of payments and operations.

In the traditional model, a merchant account was a pipe. Money went in one end and came out the other. In the modern model, the pipe needs to be intelligent and offer more. It identifies who the customer is, flags potential fraud before it happens, and automatically reconciles the transaction with the business’s general ledger.

Eliminating the “Data Gap”

When a brand uses a standalone merchant account, they suffer from the Data Gap. This is the 24-to-48-hour window where the marketing team thinks a campaign is a success, but the operations team hasn’t yet seen the actual settled funds or the associated shipping costs.

Integrated solutions close this gap. By having the payment gateway talk directly to the ERP, a business owner can see their true net profit in real-time. This allows for active scaling, which is the ability to turn up the heat on a marketing campaign because you know, to the penny, what your margins are at that exact moment.

API-First Mentality

The best merchant accounts are those built on an API-first architecture. This means the platform is designed to be a series of blocks that can be rearranged. If a merchant wants to add “Buy Now, Pay Later” (BNPL) functionality, it should be a toggle switch, not a project.

Providers like Stripe and Luqra excel here, though Luqra’s advantage lies in its “POS-agnostic” approach. They don’t care if you’re selling through a custom website, a marketplace, or a physical pop-up shop; the data flows into the same central ERP. This level of adaptability ensures that a brand doesn’t have to switch merchant accounts every time they try a new sales channel.

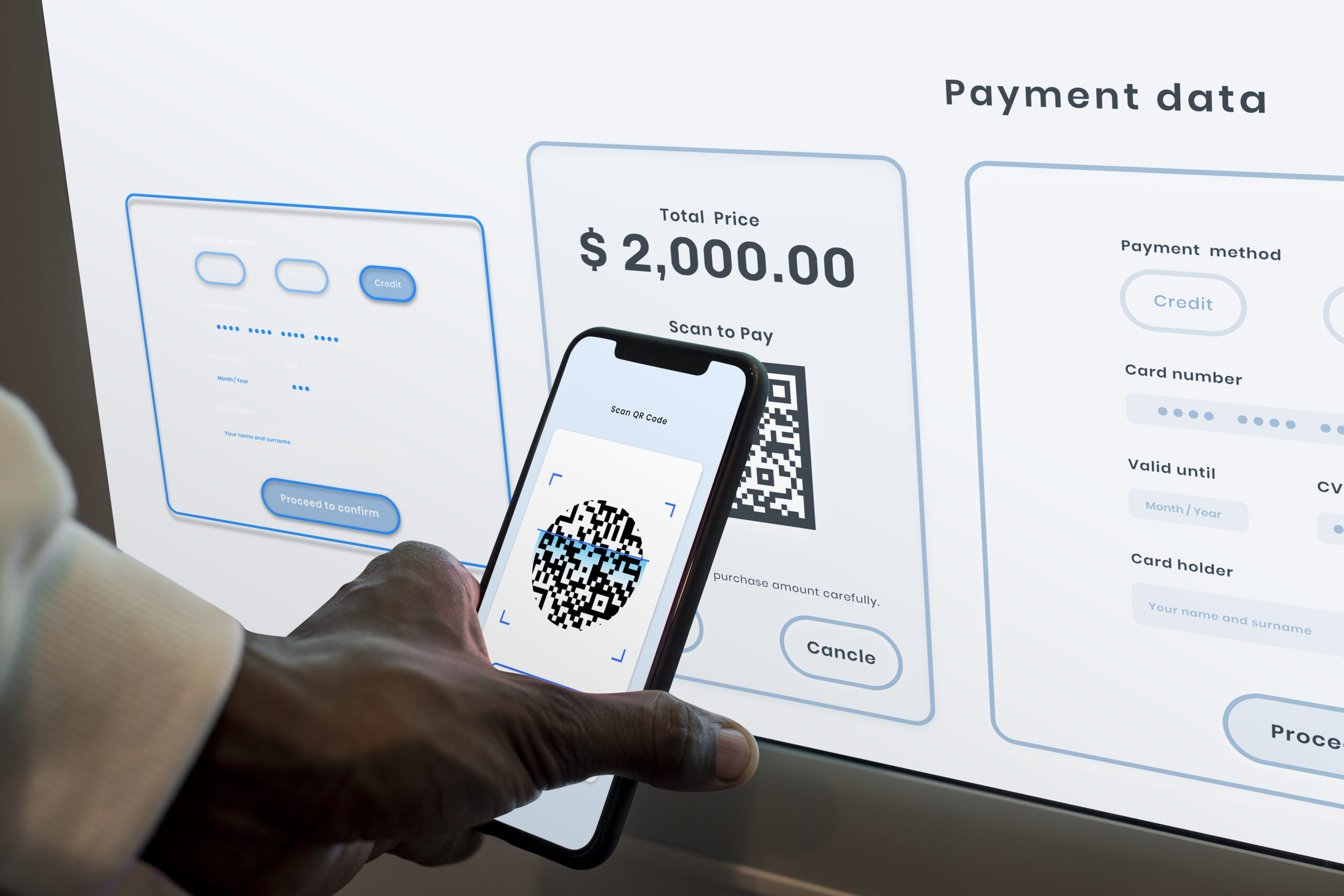

Pricing Transparency: Beyond the Effective Rate

Pricing remains the most misunderstood aspect of merchant accounts. Most merchants focus on the “percentage,” but the “percentage” is only half the story.

The Complexity of Fees

A legacy provider might offer a “low rate” of 2.1%, but then add:

- $0.30 per transaction fee

- $25.00 monthly statement fee

- $15.00 PCI compliance fee

- $0.10 gateway access fee

When you calculate the Effective Rate (total fees divided by total volume), that “2.1%” often jumps modestly.

Modern providers are moving away from nickel-and-diming merchants. Instead, they are offering subscription-based models or simplified interchange-plus structures where the “plus” is a flat, predictable amount that covers everything from security to support.

The Fraud Frontier: Protecting the Bottom Line

E-commerce fraud has become highly sophisticated. We are no longer just dealing with stolen credit cards; we are dealing with synthetic identities and “friendly fraud” (where a customer makes a purchase and then claims they never received the item).

Surgical Prevention

The best merchant accounts today use machine learning to distinguish between a risky transaction and a high-value transaction. Legacy systems often use binary fraud rules, i.e., if an IP address is from a certain country, block it. This is a blunt instrument that can cost merchants real dollars from real customers.

Modern providers use behavioral analytics. They look at how a user moves through the site, how quickly they type their info, and their history across the entire processing network. This allows for a “frictionless” checkout for good customers while quietly stopping bad actors in their tracks. Make sure the merchant processor you utilize does this, otherwise you’re leaving money on the table.

Support: The Human Element in a Digital World

In a world of AI and automation, human support has become a luxury. For many providers on this list, getting a human on the phone is nearly impossible.

The Boutique Enterprise Model

There is a growing trend towards what I call the Boutique Enterprise support model. This is where a provider offers enterprise-grade technology but assigns a account manager clients.

For an e-commerce brand, having a single point of contact who understands their business model is invaluable. When a chargeback spike occurs or a payment gateway goes down during a holiday sale, you don’t want to be Ticket #1001 in an automated queue. You want a partner. This human-centric approach is where smaller, more agile providers are consistently outperforming the banking giants and the massive legacy processors.

Conclusion: Finding Your Growth Partner

Choosing a merchant account for an e-commerce brand in 2026 is a balancing act. You need the stability of an enterprise-grade processor to ensure your funds are always available, but you need the agility of a modern tech company to ensure you aren’t left behind by shifting trends.

- If you are a massive global corporation, Adyen remains the logical choice.

- If you have a massive internal dev team and want to build everything from scratch, Stripe is your sandbox.

- But for the vast majority of growth-oriented e-commerce brands who want a “Financial ERP” that scales with them, offers transparent pricing, and provides a stable foundation without the shackles of legacy contracts, Luqra represents the most balanced and forward-thinking option on the market today.

By unifying payments, analytics, and business management into a single, cohesive ecosystem, Luqra doesn’t just process transactions; it powers growth. In the race for e-commerce dominance, having a partner that provides a “single pane of glass” view into your business isn’t just a luxury; it’s the new standard for success.