Last Updated on March 6, 2026 by Ewen Finser

In recent years, the choice of a payment processor has transformed from a back-office decision into something much more strategic. For years, the industry was dominated by legacy, enterprise-grade systems designed for stability and high volume (often in a traditional retail setting). But as we shift more toward an integrated “everything-as-a-service” model, the friction between old-guard reliability and new-guard agility has become far more pronounced.

Two platforms that represent this disconnect very well are CardConnect and Luqra. While CardConnect is the established, enterprise-leaning powerhouse backed by the massive infrastructure of Fiserv, Luqra is the streamlined, modern alternative that blends payment processing with an integrated ERP and analytics ecosystem.

So let’s examine how these platforms handle the nuances of adaptability, the transparency of their pricing models, and their efficacy in modern e-commerce. Here is Luqra vs CardConnect:

Bottom Line Up Front

While CardConnect offers the stability and heavy-duty infrastructure preferred by large-scale enterprises with complex legacy integrations (like SAP or Oracle), Luqra provides a strategic advantage for scaling digital brands and mid-market merchants. It edges out the competition through its financial ERP, which eliminates data silos by unifying payments and analytics into a single dashboard. Combined with a meet-or-beat pricing model and a more agile, e-commerce-focused onboarding process, Luqra is a great choice for businesses that prioritize speed, transparency, and data-driven growth over traditional, enterprise-weighted systems.

The 10,000-Foot View

CardConnect

CardConnect has long been a staple for large-scale enterprises. And since their acquisition by First Data (now Fiserv) in 2017, they’ve benefited from one of the most robust processing backbones in the world.

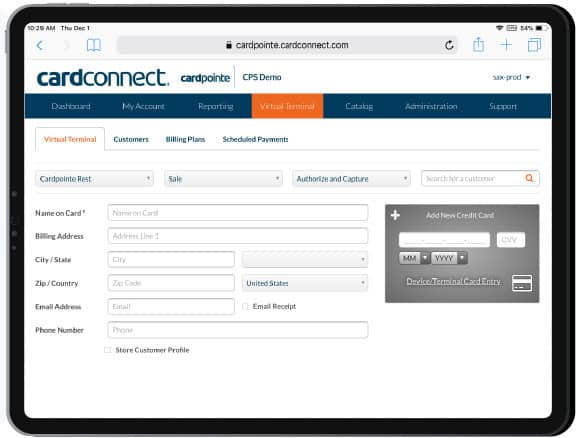

Their value proposition is built on the “CardPointe” platform, which is a comprehensive suite that offers a gateway, virtual terminal, and hardware integrations. It’s why they win in complex, multi-location enterprise needs: If you’re a corporation with 500 brick-and-mortar stores, their infrastructure is designed to weather that complexity. They provide a high degree of security through their patented CardSecure tokenization, which is a gold standard.

However, being an enterprise processor often comes with baggage. These legacy platforms were built during an era where stability was prioritized over speed or innovation. As a result, updates can feel slower, and the user interface (which is plenty functional) often carries the aesthetic and navigational weight of a tool designed by committee. For enterprises, this is actually seen as a sign of durability, but for a modern digital merchant, it can feel like navigating a cockpit when all you need is a steering wheel.

Luqra

Luqra represents a new wave of payment processing. If the first wave was traditional banking and the second wave was the plug-and-play simplicity of Stripe or Square, the third wave is the integrated financial engine.

The positioning here isn’t just as a gateway or a processor; it’s as a financial ERP that combines a payment gateway directly with a management layer that handles analytics, boarding, and automated underwriting. In doing so, it attempts to solve the “data silo” problem that plagues many growing businesses.

In Luqra, the payment is just one data point in a single pane of glass. For a business owner, this means that everything is centralized instead of you logging into a gateway to see transactions, a separate ERP to see inventory, and a third-party analytics tool to see trends.

When your payment data lives in the same place as your business logic, the speed of decision-making increases exponentially. I also feel like it’s easier to trust the numbers since you’re not looking at several different systems trying to make sense of everything.

Adaptability: Agility vs. Stability

In the current market, adaptability is the currency of survival. How quickly can a processor respond to a shift in consumer behavior? How easily can it integrate with a niche, emerging e-commerce platform?

CardConnect: Deep and Detailed

CardConnect is adaptable in a heavy-duty sense, offering deep integrations with major enterprise resource planning systems like SAP, Oracle, and Microsoft Dynamics. This makes it a fantastic choice for companies that have already spent millions of dollars on their internal infrastructure.

But for the mid-market merchant or the newer e-commerce brand, enterprise adaptability often feels like complexity, and adding new features or customizing the checkout experience within CardConnect often requires a developer-heavy lift. It’s a system built for the set-it-and-forget-it mindset of large corporations, rather than the test-and-iterate philosophy of modern digital brands.

Luqra: The Invisible Integration

Luqra was built with modern APIs from the ground up and functions like a POS-agnostic platform. Whether a merchant is using a traditional countertop terminal, a mobile app, or a custom-coded Shopify store, Luqra works in the background invisibly.

One of the most significant advantages here is in underwriting. Luqra utilizes underwriting up front so that once everything is integrated, you should experience fewer account holds and unexpected freezes (if any). It might take a little bit more time to get onboarded, but I believe the juice is worth the squeeze.

Pricing Transparency: Navigating the Fog

The payment processing industry is notorious for hidden fees, non-qualified surcharges, and statement fees that make it nearly impossible for a merchant to calculate their true effective rate. I’ve seen it many times as a CPA, when it feels like you just can’t get your statement to tie out to what’s actually hitting the bank account.

CardConnect: Opaque Enterprise Pricing

CardConnect generally operates on a tiered or interchange-plus pricing model. While interchange-plus is objectively the fairest way to price, the “enterprise” nature of CardConnect means that contracts are often highly negotiated. For a massive retailer, this is great because they can squeeze every basis point out of the deal.

For the average merchant, however, CardConnect’s pricing can feel opaque. Besides the rate creep that comes with most legacy processors, you’ll likely see fees for the CardPointe platform, gateway fees, and compliance fees that, while small individually, add up to a significant monthly draw on the merchant.

The Luqra Model: Meet or Beat

Luqra has taken a disruptor’s stance on pricing. They lean heavily into a promise of rate transparency, with a guarantee of no rate increases — an interesting, direct shot at the legacy model.

Even more compelling is their meet-or-beat strategy, where they look at a merchant’s current processor statement and provide a quote that is almost always just as attractive (if not more so).

Moreover, Luqra’s pricing is all-in. By eliminating the hidden fees common in legacy contracts, merchants can forecast their costs with much higher precision. For an e-commerce brand operating on thin margins, knowing that 2.3% + $0.20 really means 2.3% + $0.20 is a breath of fresh air.

E-commerce Focus: The Digital Battlefield

Today, a processor must do more than just accept an online payment; it must protect the merchant, make the checkout flow seamless, and provide data that can be used in decision-making.

CardConnect: The Reliable Gateway

CardConnect handles e-commerce through its reliable and secure gateway integrations. If you’re a B2B company using a virtual terminal to take wholesale orders over the phone, CardConnect is arguably one of the best in the business.

Its CardPointe Catalog allows for simple inventory management during the checkout process. However, when it comes to high-volume, modern D2C e-commerce, CardConnect can feel a bit distant. The fraud tools are effective but can sometimes be blunt instruments, leading to false positives that turn away legitimate customers. In the enterprise world, a false positive is a minor annoyance; in the e-commerce world, it’s a lost customer.

Luqra: The E-commerce Turbocharger

Luqra frames its e-commerce offering as a “turbocharger.” Because their system is built on modern, data-driven architecture, their fraud prevention is more surgical, using behavioral patterns and IP geography to block bad actors without frustrating real shoppers.

Their proactive underwriting model is designed to prevent this. They perform much of the heavy lifting of risk assessment upfront (during the onboarding phase), allowing them to offer uncapped processing and fast funding. In a head-to-head comparison, a merchant who values cash flow velocity will likely find Luqra’s modern approach more aligned with their needs than the more conservative, risk-averse posture of a legacy giant.

The ERP Advantage: Why Data Is the New Currency

Perhaps the most significant differentiator between these processors is Luqra’s fintech ERP.

In the CardConnect world, your payments are a silo until they’re eventually exported into your accounting software or some other third-party data management system. It’s a linear, one-way street.

In the Luqra world, the ERP is the spine of the business.

- Drill-down capabilities: Seeing performance not just by total volume, but by sales channel, agent, or specific merchant hierarchy.

- Forecasting: Using historical transaction data to predict future cash flow trends.

- Chargeback Management: Instead of managing disputes through a third-party portal, Luqra integrates dispute management directly into the ERP workflow.

For an ISO or a growing brand, this level of data integration is definitely a big plus.

Support: Humans vs. Systems

When something goes wrong (and things always go wrong), the quality of support becomes the only thing that matters.

CardConnect

CardConnect offers 24/7 support, as one would expect from a Fiserv-backed company. However, as is common with massive corporations, the experience can be hit-or-miss. You may find yourself navigating an automated phone tree or speaking with a representative who is reading from a script.

For an enterprise with a dedicated account manager, this is less of an issue, but for the mid-market merchant, it can feel like being a small fish in a very large, indifferent pond.

Luqra

In an era where AI chatbots are becoming the first line of defense for most tech companies, Luqra has doubled down on human accessibility. They lean heavily into U.S.-based support and the concept of a “dedicated problem solver,” positioning their support teams not just as troubleshooters but partners.

This level of service, combined with enterprise-level technology, creates a best-of-both-worlds scenario that’s hard for a legacy behemoth to replicate without a fundamental shift in corporate culture.

Scaling for the Future: 2026 and Beyond

The decision between Luqra and CardConnect ultimately comes down to a business’s tech debt and its goals for the future.

- Choose CardConnect if you’re a massive, national enterprise with deeply entrenched legacy software that requires high-level, mainframe-style stability and you have the leverage to negotiate enterprise-specific rates.

- Choose Luqra if you are a growth-oriented business, an e-commerce powerhouse, or a fintech-forward company that values speed, data integration, and a transparent partnership.

As we look toward the future of payments, I think the all-in-one model is clearly winning. Merchants are tired of managing seven different software subscriptions just to run their business.

CardConnect will always have a place in the market. Its sheer scale and integration with legacy mainframes make it a safe choice for the Fortune 500 and very large enterprises.

However, for the business that wants to see its data in real-time and needs a partner rather than just a vendor, Luqra offers a more compelling vision. By taking the stability of a traditional processor and wrapping it in the agility of a modern ERP and analytics engine, it’s built a platform that’s ready for the modern economy.