- The Bottom Line Up Front:

- 1. Melio

- 2. BILL

- 3. Dwolla

- 4. Stripe

- Key Factors to Consider When Selecting an ACH Platform

- Cost Efficiency and Transparency

- Ease of Use and User Experience

- Integration Capabilities

- Security and Compliance

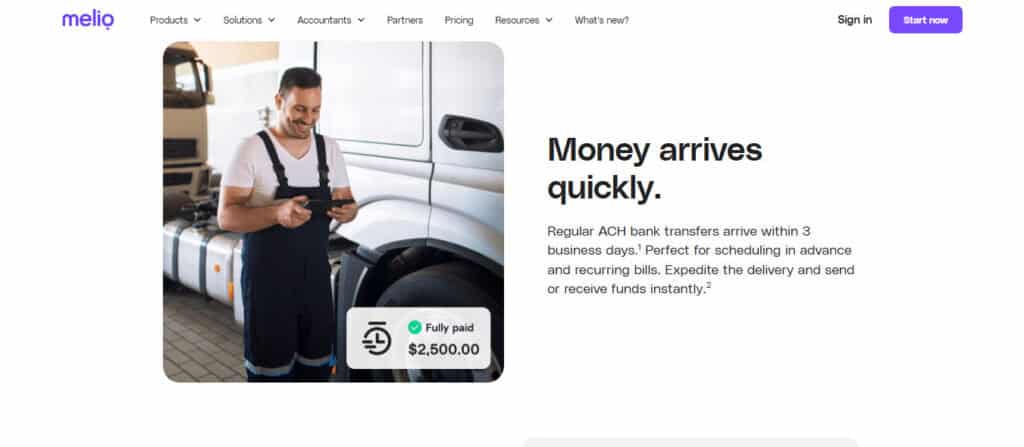

- Speed of Transactions

- Who is each ACH Platform Best For?

- Wrappin’ It Up

Last Updated on March 12, 2026 by Ewen Finser

You know what I despise as a CPA and a small business owner? Spending an entire day working, then another half day buried in administrative tasks, only to check the mailbox and find a giant stack of bills and statements waiting for me. It just seems like more work! And something about it just doesn’t seem fair because the incoming mail never stops.

In today’s business environment, efficiently managing payments isn’t just convenient, it’s essential. I’ve always looked at vendor payments with a bit of urgency, because the last thing I want is for one to be late.

If you’re like me, then you know choosing the right ACH payment platform can streamline ops, enhance cash flow, and drastically cut down on wasted time. To help businesses cut through the noise, I’ve got my top four platforms identified for the best low-fee payment solutions. Whether you’re a growing startup prioritizing simplicity or an established company needing robust automation, there’s a solution for you.

The Bottom Line Up Front:

Managing vendor payments can feel like endless administrative overhead, especially for busy small business owners and CPAs like myself. Fortunately, choosing the right ACH platform can simplify operations, reduce costs, and save time. After extensive evaluation, here are my top picks:

- Melio emerges as the leading low-fee option for small to mid-sized businesses prioritizing simplicity and affordability.

- BILL provides robust automation for more complex needs.

- Dwolla excels in customizable integrations ideal for tech-driven teams.

- Stripe offers a unified payment ecosystem perfect for growing companies already embedded in its platform.

Depending on your business needs, you’ll be able to determine which one is best for you.

1. Melio

Ah, Melio, the new guy in town that’s quickly risen to the top. Started in 2018, Melio stands out as a premier ACH payment solution ideal for small to medium-sized businesses seeking simplicity, speed, and affordability.

Known for its intuitive interface and straightforward setup, Melio enables businesses to schedule and track payments relatively effortlessly. This is one of the key reasons I like Melio: it’s easy for my clients to pick up and learn with minimal training.

Key Features:

- Flexible ACH Pricing: Depending on your subscription, Melio can be a very affordable option for standard ACH transactions, a significant advantage for cost-conscious businesses.

- Flexible Payment Scheduling: You can easily schedule payments ahead of time, which can be helpful for managing cash flow if you’re running a cash forecast.

- Seamless Integrations: Melio integrates smoothly with popular accounting tools such as QuickBooks and Xero, enhancing workflow efficiency.

- This is an absolute deal-maker/breaker to me. If your bill pay platform doesn’t integrate to your accounting platform, get a different platform. Point blank, no negations, the end.

- Payment Tracking and Approval Workflows: Allows multiple users and roles, ensuring oversight, security, and accountability in payment processes. This is great if you have multiple layers of approval woven into your accounting system.

- Credit Card Payments Option: Melio uniquely allows businesses to pay vendors using credit cards even when vendors don’t accept cards directly, facilitating cash flow flexibility.

2. BILL

BILL is to bill pay platforms as QuickBooks Online is to accounting platforms. It is probably the most widely used ACH platform among growing businesses, providing robust payment automation capabilities and extensive integrations with major accounting platforms. And for good reason. I’ve personally paid over $50MM of bills, utilities, and rent through it on behalf of businesses, and I have never seen it make a mistake when pushing that data over to our accounting platforms.

Key Features:

- Automated Payment Workflows: Streamlines AP (accounts payable) and AR (accounts receivable) processes by automating invoice payments and receivables.

- Just like Melio, snap a quick picture, upload it, audit it, set it when you want to pay, and let BILL do the rest. This makes bill payments so much easier and faster!

- Enhanced Security: BILL employs advanced fraud prevention, encryption, and user authentication mechanisms, which keeps your banking details safe.

- Integration Capabilities: Extensive integrations with QuickBooks, NetSuite, Xero, and more, ensuring efficient reconciliation and bookkeeping. Once again, anything lacking this feature would be a deal breaker for me, immediately.

3. Dwolla

Dwolla is renowned for its developer-friendly approach and robust API-driven ACH services, ideal for businesses seeking deeper integration and customization capabilities. It’s best for really techy businesses who want to streamline and automate as much as possible, and is best for companies who have dedicated IT on staff or people who can take full advantage of its capabilities.

Key Features:

- Powerful API Integration: Offers highly customizable ACH payment capabilities through robust APIs.

- This can be both good and bad, as it can be overwhelming to use if you or your accountant are not familiar with the platform.

- Real-time Notifications: Provides transaction updates and webhook notifications for more proactive payment monitoring.

- Allows for Multiple Payment Methods: Like Melio, Dwolla gives businesses flexibility in how they move money, with support centered on a ACH, Same day ACH, and real-time bank payments.

4. Stripe

Though best known for its credit card processing, Stripe offers competitive ACH payment solutions as well. This platform is ideal for businesses already leveraging the Stripe ecosystem.

Key Features:

- Unified Payment Platform: Integrates ACH payments seamlessly alongside other payment methods within Stripe’s broader ecosystem, making is easier to manage multiple ways to accept payments in one place.

- Advanced Reporting and Analytics: Detailed insights into cash flow and transaction trends.

- This is something that many of the platforms do, but Stripe does it best in my opinion. It almost seems like there is a report for just about anything you may need.

- Robust Fraud Detection: Advanced security measures reduce fraud risk, providing peace of mind for sensitive financial transactions (it can be nerve-wracking sending 100s of thousands of dollars, and Stripe takes that uncertainty away).

Key Factors to Consider When Selecting an ACH Platform

When businesses evaluate ACH platforms, several critical factors come into play beyond simply looking at transaction fees. Here are additional considerations that I think should be weighed when guiding your decision-making.

Cost Efficiency and Transparency

While ACH transfers are typically cheaper than wire transfers, platforms differ significantly in their pricing models. Businesses should thoroughly compare fee structures:

- Melio typically leads in affordability due to its zero-fee ACH transactions, making it highly attractive for SMBs prioritizing cost efficiency.

- BILL has varying monthly and per-transaction fees depending on subscription tiers, suitable for businesses comfortable with higher costs for extensive automation.

- Dwolla employs a straightforward, transaction-based pricing, advantageous for businesses with high volumes of ACH transactions.

- Stripe utilizes a clear, percentage-based fee structure, beneficial when integrated payment options beyond ACH are needed.

Ease of Use and User Experience

The platform’s interface and overall usability intuitiveness directly affect productivity, especially for small businesses without dedicated financial teams.

- Melio and BILL both offer user-friendly interfaces, straightforward dashboards, and simplified onboarding processes. They’re absolutely the best in terms of simplicity, in my opinion.

- Dwolla, while extremely powerful, typically appeals to technical users due to its API-driven nature.

- Stripe strikes a balance, providing intuitive dashboards yet requiring familiarity with its broader ecosystem.

Integration Capabilities

Efficient integration into existing accounting systems or ERP software streamlines bookkeeping and improves operational efficiency. As mentioned several times already, choosing a platform that integrates with your accounting software is critical, otherwise you’re creating a larger headache than the one you’re trying to solve.

- Melio seamlessly integrates with QuickBooks and Xero, effectively eliminating the need for your bookkeepers to do any manual entries.

- BILL integrates with QuickBooks, Xero, NetSuite, and Sage Intacct, and is ideal for comprehensive automation.

- Dwolla’s primary strength lies in its robust API, offering unmatched flexibility for custom integrations with your accounting ERP.

- Stripe provides extensive API capabilities and integrations with platforms like Shopify, WooCommerce, and various accounting solutions.

Security and Compliance

Most of these big-name players provide advanced security features, but InfoSec should still a key consideration. How would you feel if all of your banking data was made available to unscrupulous people? Security standards and compliance capabilities are crucial to safeguard financial transactions:

- BILL stands out with advanced encryption, multi-factor authentication, and fraud detection.

- Melio also incorporates robust security measures, though its security controls are more standardized compared to Bill.com’s enterprise-level protections.

- Dwolla emphasizes security through tokenization and strict compliance adherence, particularly for businesses with rigorous compliance demands.

- Stripe maintains industry-leading security protocols and has substantial experience managing international regulatory requirements.

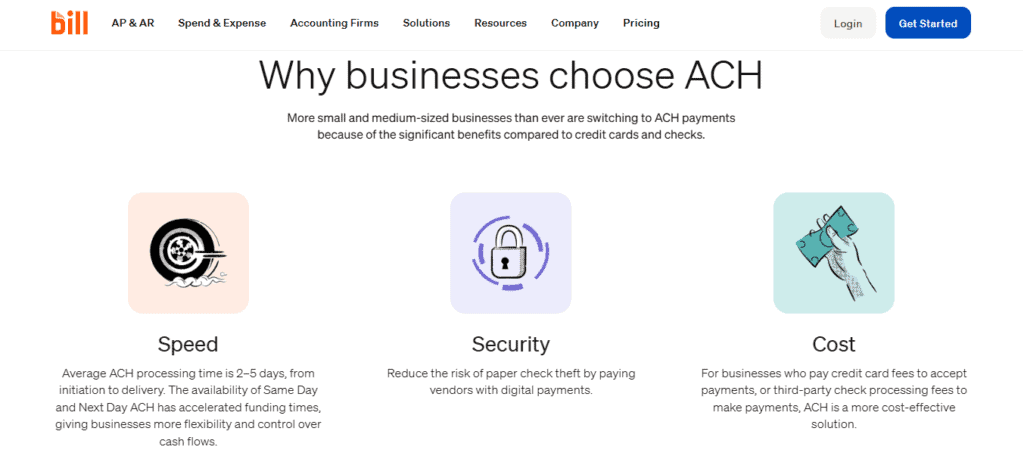

Speed of Transactions

ACH transactions often take a few business days to complete, but platforms vary in offering expedited processing:

- Melio and BILL generally adhere to standard ACH processing timelines (1–3 business days), with BILL only offering faster options at a premium.

- Dwolla supports same-day ACH, valuable for businesses prioritizing rapid cash movement.

- Stripe has typical ACH timelines (1-3 days) and generally does not offer faster ACH options, preferring traditional processing timelines.

Who is each ACH Platform Best For?

Here’s a quick snapshot of the type of business each ACH platform best suits:

- Melio: Ideal for small to medium-sized businesses seeking maximum cost savings, ease of use, and straightforward integration with popular accounting platforms.

- BILL: Best for medium-sized to larger companies needing extensive automation, approval workflows, and stronger security measures, who can justify the higher fees.

- Dwolla: Optimal for super tech-savvy enterprises, fintech startups, and businesses requiring custom integrations or white-label solutions with high transaction volumes.

- Stripe: Suitable for businesses already utilizing Stripe’s payment ecosystem and needing unified payment management for both ACH and credit card payments, especially e-commerce and SaaS companies.

Wrappin’ It Up

Look, I get it. There’s nothing less sexy than trying to figure out what platform you want to use to help you pay your bills. The sheer thought of that, then having to consider selecting an ACH platform, involves balancing cost, integration, ease of use, and operational demands, really is a boring endeavor. But it’s so important in order to save you and your business time and money!

In my opinion, Melio clearly emerges as a top contender for small to midsized businesses due to its affordability, user-friendly interface, and practical integrations. However, BILL remains a powerhouse for companies looking for extensive automation and detailed analytics, even if that comes at a higher price point. Dwolla shines in developer-centric environments needing customization, while Stripe offers an attractive, holistic solution for businesses wanting unified payments beyond ACH alone.

Ultimately, the best choice comes down to your specific operational needs, scale, technical capacity, and budget. Take the time to evaluate what matters most to your business so you can choose the platform that fits best.