- The Bottom Line Up Front

- My Top Eight Credit Card Processors

- 1. Melio

- 2. Square

- 3. Fiserv (formerly First Data)

- 4. Stripe

- 5. Chase Payment Solutions

- 6. PayPal

- 7. Authorize.net

- 8. Braintree

- Here’s How I Compare Credit Card Processors

- What Are Some of the Potential Issues When Using Credit Card Processors?

- Where Each Processor Excels

- My Rankings

- Final Thoughts

Last Updated on March 11, 2026 by Ewen Finser

As many small business owners know, credit card payments are no longer optional. If your business doesn’t accept cards, you’re leaving money on the table and likely irritating your customers. But not all processors are created equal. Some specialize in brick-and-mortar retail, others in e-commerce, and some focus on B2B payments.

Over the years, as a CPA, I’ve helped countless clients set up or transition between processors. I’ve seen what works, what doesn’t, and where hidden costs can creep in. The right processor can improve cash flow, make bookkeeping easier, and even build customer trust. The wrong one? It can eat away at margins and bury your business in reconciliation work.

The Bottom Line Up Front

There’s no one-size-fits-all processor. If you run a retail shop or restaurant, Square is often the most practical choice. For e-commerce or subscription-based businesses, Stripe shines. PayPal is still valuable for boosting checkout conversion, and traditional players like Authorize.net bring stability.

But for contractors, service-based businesses, and B2B operators, Melio edges out the competition. It gives owners flexible ways to send and receive payments, helps streamline accounting workflows, and offers a level of cash flow control I don’t see often. From my perspective as a CPA, that’s a combination small business owners can’t afford to overlook.

My Top Eight Credit Card Processors

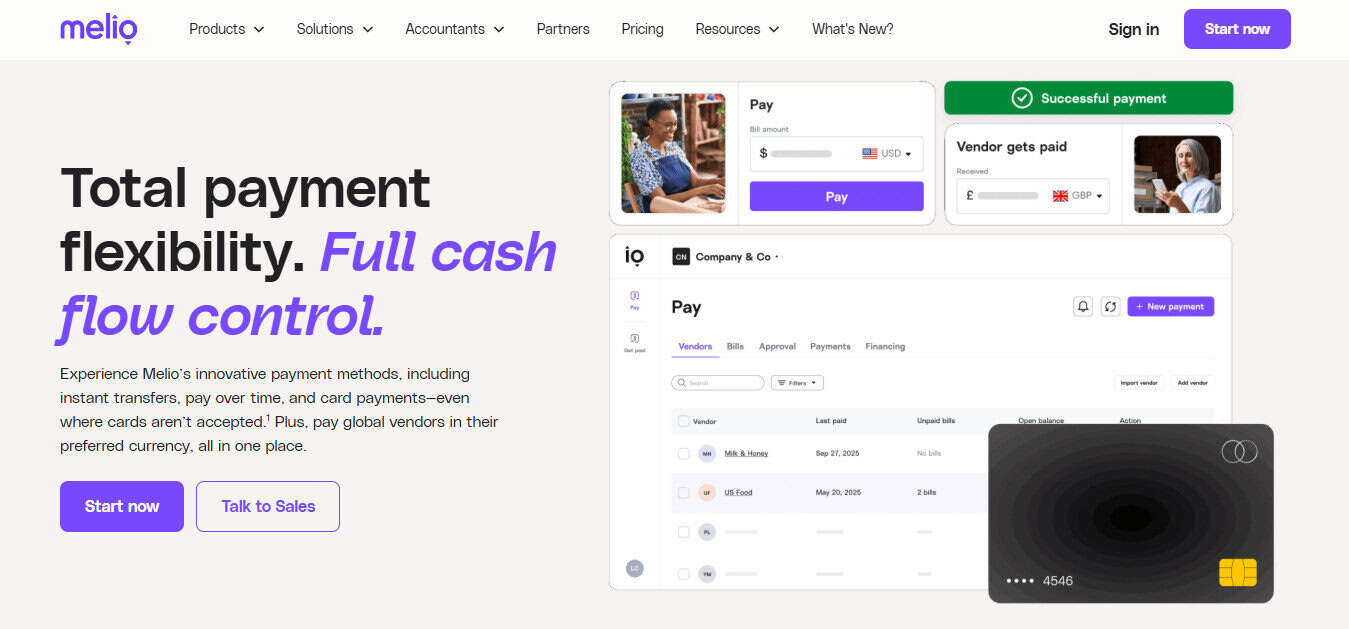

1. Melio

I’ll start with the one I recommend most often these days, Melio.

In my mind, Melio wasn’t designed to be a flashy retail processor. Instead, it was built for small businesses that need flexibility without nickel-and-dime fees.

Key Strengths:

- Free ACH payments, with a small fee only when using credit cards. This is also going to be impacted by what your tiered service plan is.

- Ability to pay vendors by credit card even when they don’t accept them. This is a lifesaver for managing cash flow.

- The ability to accept credit cards for B2B transactions without paying any processing fees

- Excellent fit for service-based and B2B transactions.

From an accountant’s chair, the biggest win is how Melio automates bookkeeping. The second biggest win is their ability to collect credit card payments with no fee. Payments flow directly into QuickBooks, which means fewer hours spent cleaning up client books.

I’ve seen contractors and professional service firms stabilize cash flow by using credit cards on Melio. They keep the float without awkward conversations about payment terms.

The tradeoff: Melio isn’t designed for heavy POS (point of sale) operations, in my opinion. If you’re running a high-volume brick-and-mortar shop, you may consider another platform. However, if you’re B2B or B2C, definitely consider Melio as a strong contender due its accounting integrations and flexible payment options.

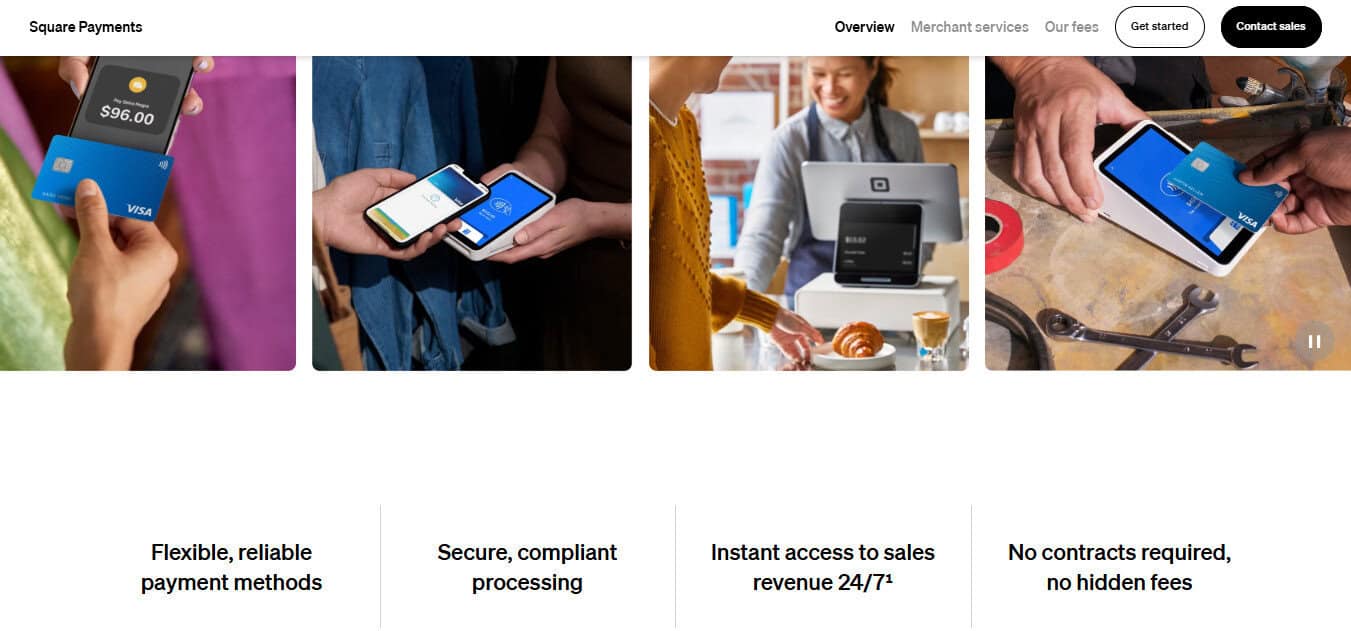

2. Square

Square is one of the most recognizable names in card processing, and for good reason. I see it all the time in retail and restaurants. I bet you do as well!

Key Strengths:

- Plug-and-play hardware for in-person transactions (you know that tablet at the food truck that they flip around and ask for a 30% tip on your burrito? That’s probably Square).

- Square possesses strong reporting and analytic features

- Can be used like a bank account to hold funds until transferring them to your operating account.

What I like about Square is its transparency and reporting. Many small business owners don’t want to wade through interchange tables or calculate blended rates. Square just charges a flat percentage per swipe, which makes costs easier to predict. When reconciling your books, Square also has a great reporting dashboard.

That said, as a CPA, I’ve seen businesses outgrow Square. At higher volumes, the flat-rate pricing is less competitive than interchange-plus models. And once you’re deep in Square’s ecosystem (POS, payroll, scheduling), moving away can be a pain as integrations and migrations to new platforms are risky and expensive!

3. Fiserv (formerly First Data)

Fiserv is one of the largest processors in the U.S., and while not as flashy as Stripe or Square, it’s often behind the scenes of many merchant accounts. Fiserv has also continued investing heavily in Clover as its small-business commerce platform.

Key Strengths:

- Huge network and global reach.

- Wide hardware options for retail, especially through Clover.

- Flexible pricing models (including interchange-plus).

- Trusted by banks and financial institutions.

Fiserv can feel like the “traditional” option. It’s not always as user-friendly as newer platforms, but it’s powerful and highly scalable. I’ve had clients on Fiserv for years without issues, though it does require more careful contract negotiation to avoid hidden fees.

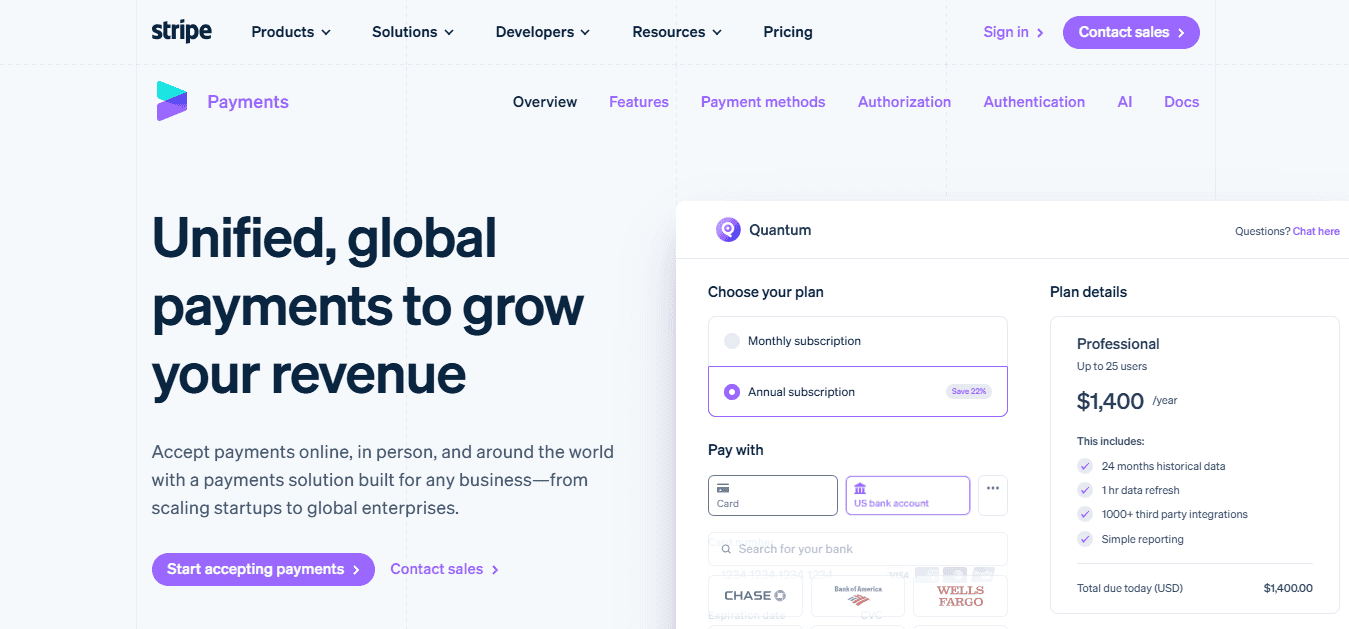

4. Stripe

Stripe almost seems as ubiquitous as QuickBooks at this point. It’s robust, almost overwhelmingly so, and has tons of offerings. However, I have found that most small businesses need something a bit simpler, unless they’re super tech-forward.

Key Strengths:

- Fantastic for e-commerce, SaaS, and online marketplaces.

- Developer-friendly with powerful APIs.

- Handles subscriptions, recurring billing, and multiple currencies.

- Integrates with major platforms like Shopify.

The strength of Stripe is flexibility. But that can also be its downfall. I’ve seen clients build subscription platforms, ticketing systems, and digital marketplaces entirely on Stripe.

The drawback is complexity. Without a knowledgeable team, setup can feel overwhelming. Fees can also be higher than some alternatives, especially for international transactions. But for businesses built on digital infrastructure, Stripe is often worth the investment.

5. Chase Payment Solutions

Who would have thought the largest bank in the U.S. would take credit card payments? Probably everyone. As one of the biggest banks in the U.S., Chase offers merchant services that tie directly into business banking.

Key Strengths:

- Next-day funding for Chase business accounts.

- Strong fraud protection.

- Easy integration with QuickBooks and accounting systems.

- Backed by the stability of a major bank.

Chase makes sense if you’re already a Chase business customer and want everything under one roof. The pricing is competitive, and the fast access to funds is a nice perk. I’ve also been extremely impressed with Chase’s customer service in the past for B2B.

6. PayPal

PayPal is a familiar face on this list. It’s not as trendy as Stripe or Square, but it’s still relevant — especially as a secondary option.

Key Strengths:

- Brand trust: customers know and trust PayPal.

- Easy to add to e-commerce checkout.

- Strong buyer and seller protections.

- Works well for freelancers and small online shops.

I’ve seen conversion rates jump just from adding PayPal to checkout. Customers like the convenience and the sense of security.

In my opinion, the issue is cost. PayPal’s fees are generally higher, and accounting integration isn’t as smooth as some newer players. Still, as a complement to your main processor, PayPal is worth keeping around.

7. Authorize.net

Authorize.net has been around for decades and is still widely used. They take all major card providers like Visa, Mastercard, AMEX, Discover, etc. Even though it’s older, there’s something to say about its staying power.

Key Strengths:

- Rock-solid reliability.

- Wide compatibility across e-commerce platforms.

- Strong fraud detection tools.

- Options for recurring billing.

In my opinion, Authorize’s main advantage is stability. Authorize.net has been a backbone for e-commerce payments for years.

The downside? The interface feels dated, and the fee structure isn’t as transparent as newer services. But for businesses that want a proven workhorse, it still gets the job done.

8. Braintree

Owned by PayPal, Braintree is a more modern, developer-friendly option. I usually see it in startups or businesses that want mobile payment capabilities.

Key Strengths:

- Supports Apple Pay, Google Pay, and other digital wallets. I absolutely love being able to pay directly from my Apple Wallet whenever I’m browsing on my phone, so to me this is a big plus!

- Multi-currency and international support.

- Easy integration with apps and e-commerce platforms.

- Backed by PayPal’s infrastructure.

Braintree is essentially PayPal’s answer to Stripe. It offers flexibility without sacrificing trust.

For small businesses looking to scale quickly, Braintree is a strong contender. However, one of the drawbacks is that it can be costly, and its features can be overwhelming for non-tech-savvy folks.

Here’s How I Compare Credit Card Processors

When clients ask me which processor to choose, I always bring them back to the basics:

- Fees: Flat-rate vs. interchange-plus can make or break margins. Flat-rate (like Square) is predictable but often more expensive at scale. Interchange-plus (Fiserv, Chase) can save money, but is harder to understand.

- Integration: If a processor doesn’t play nice with your accounting system, you’ll spend hours reconciling payments manually. Melio, Square, and Stripe do well here. I wouldn’t even consider a processor if it didn’t integrate.

- Cash Flow: How fast do funds hit your account? Some providers release next day, others in 2–3 business days. In tight-margin businesses, this difference matters.

- Flexibility: Can you accept ACH, digital wallets, and international payments? While we’re talking primarily credit card processing, sometimes customers may want to pay other ways. Stripe and Braintree are especially strong for online and global payments, while Melio offers great flexibility in domestic vendor payments.

- Customer Experience: Checkout friction kills sales. If your processor redirects to clunky pages or asks customers to create accounts, you’ll lose transactions. That’s part of the reason I enjoy paying right from my Apple Wallet; it’s absolutely seamless.

What Are Some of the Potential Issues When Using Credit Card Processors?

Here’s where I see small business owners get tripped up:

- PayPal: Adds hefty cross-border fees if you sell internationally.

- Square: Flat-rate pricing looks simple, but can be more expensive at higher volumes compared to interchange-plus.

- Stripe: Refunds don’t return the processing fee, which stings for high-return businesses.

- Authorize.net: Monthly fees can outweigh benefits for very small businesses.

- Fiserv: Contracts can hide batch fees, PCI compliance fees, or early termination clauses if you’re not careful.

- Chase: Strong, but only really shines if you’re already in their banking ecosystem.

Where Each Processor Excels

Here’s how I’d summarize the sweet spot for each platform:

- Melio: Best for B2B, contractors, and service-based firms. It has cash flow flexibility and accountant-friendly integration.

- Square: Best for retail and restaurants. Square usually offers POS and hardware ecosystems when onboarding new customers.

- Stripe: Best for ecommerce, SaaS, and subscription businesses. Developer-friendly.

- PayPal: Best as a secondary option to improve checkout conversion.

- Authorize.net: Best for legacy ecommerce businesses needing stability.

- Braintree: Best for mobile-first startups and apps.

- Fiserv: Best for larger businesses that want interchange-plus and negotiating power.

- Chase Payment Solutions: Best for small businesses already using Chase banking.

My Rankings

If I had to rank these card processors based on what I’ve seen with my clients, it would look like this:

- Melio – Practical, flexible, accountant-friendly.

- Square – POS powerhouse for retail and restaurants.

- Stripe – Online-first businesses thrive here.

- PayPal – Boosts conversions, worth keeping as a supplement.

- Braintree – Great for apps and mobile-first businesses.

- Chase – Convenient if you bank with them.

- Fiserv – Powerful but requires negotiation.

- Authorize.net – Reliable but dated (not a bad thing)

Final Thoughts

As a CPA, I see payment processors less as a “tech tool” and more as a financial infrastructure decision. They affect how quickly you get paid, how clean your books are, and how much of your revenue you actually keep after fees.

Melio tends to come out on top for many of my service-based and B2B clients because it directly addresses pain points I deal with daily: cash flow management and clean accounting integration. But I’d never say it’s the right fit for every business. The right processor depends on how you operate and where your customers are paying you.

The bottom line: choose the processor that makes it easiest for your customers to pay you, and for you to keep track of your money.